26

Capstone slides

Structured for a teacher-facing defense of decisions, evidence, trade-offs, and gaps.

7

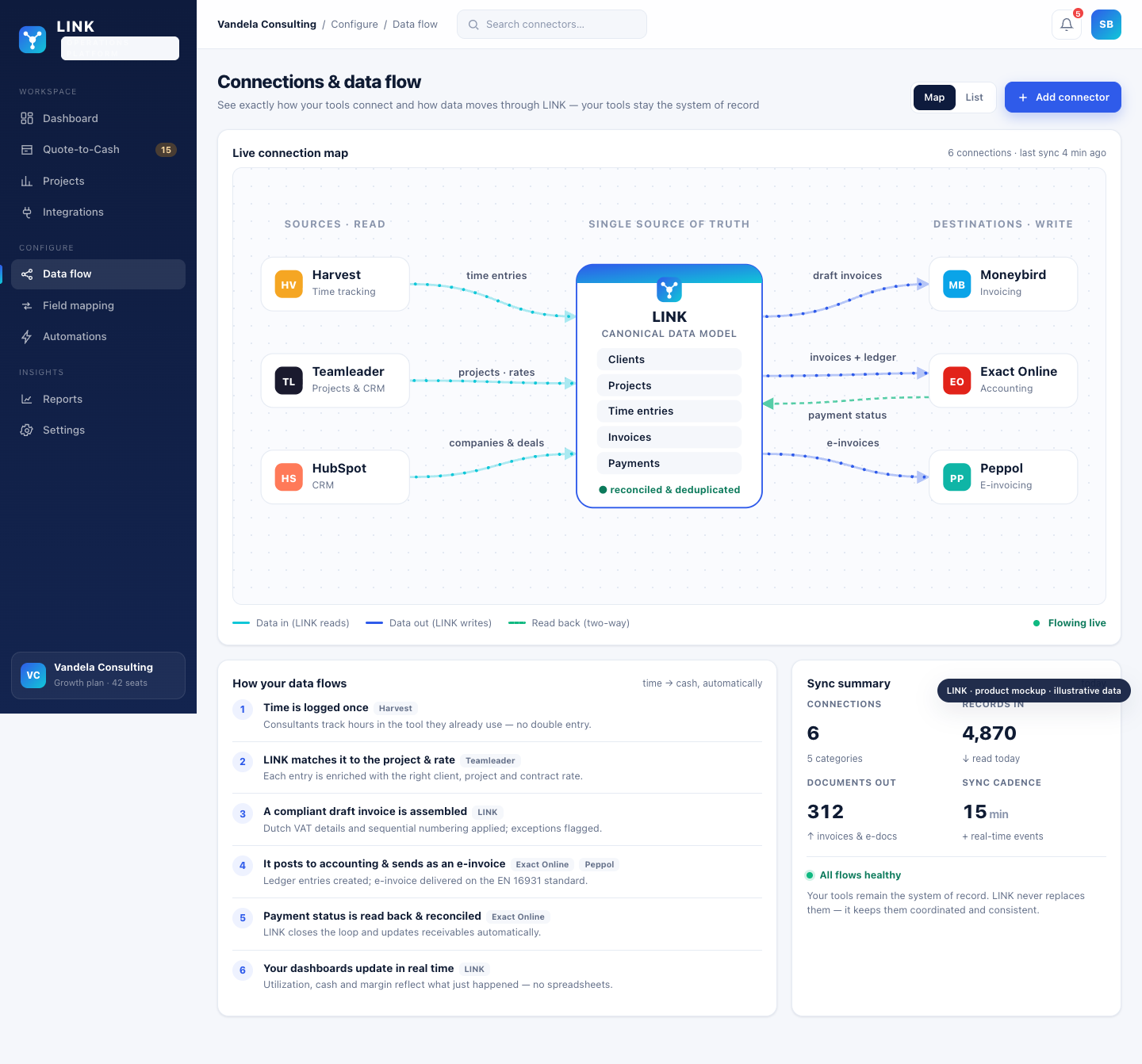

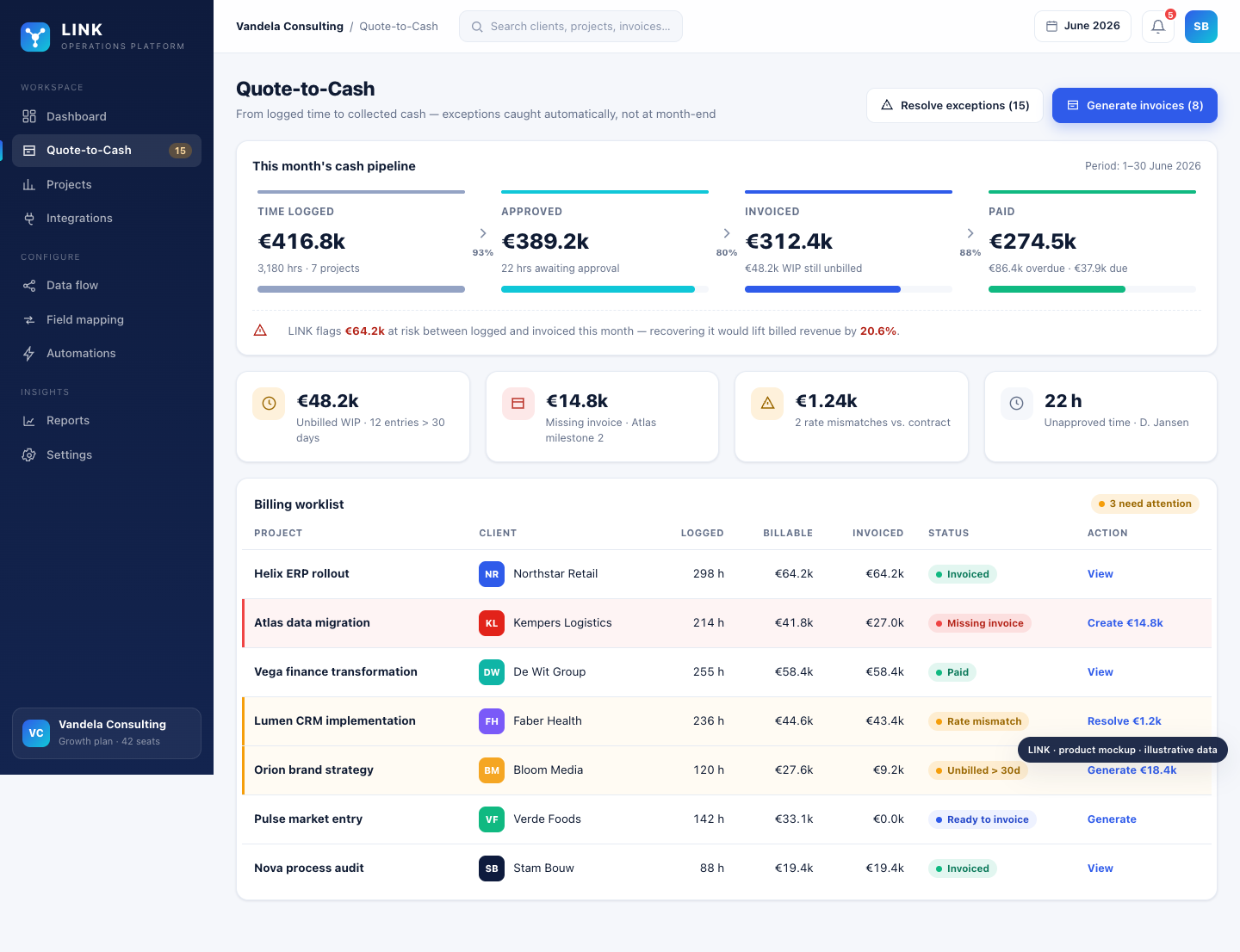

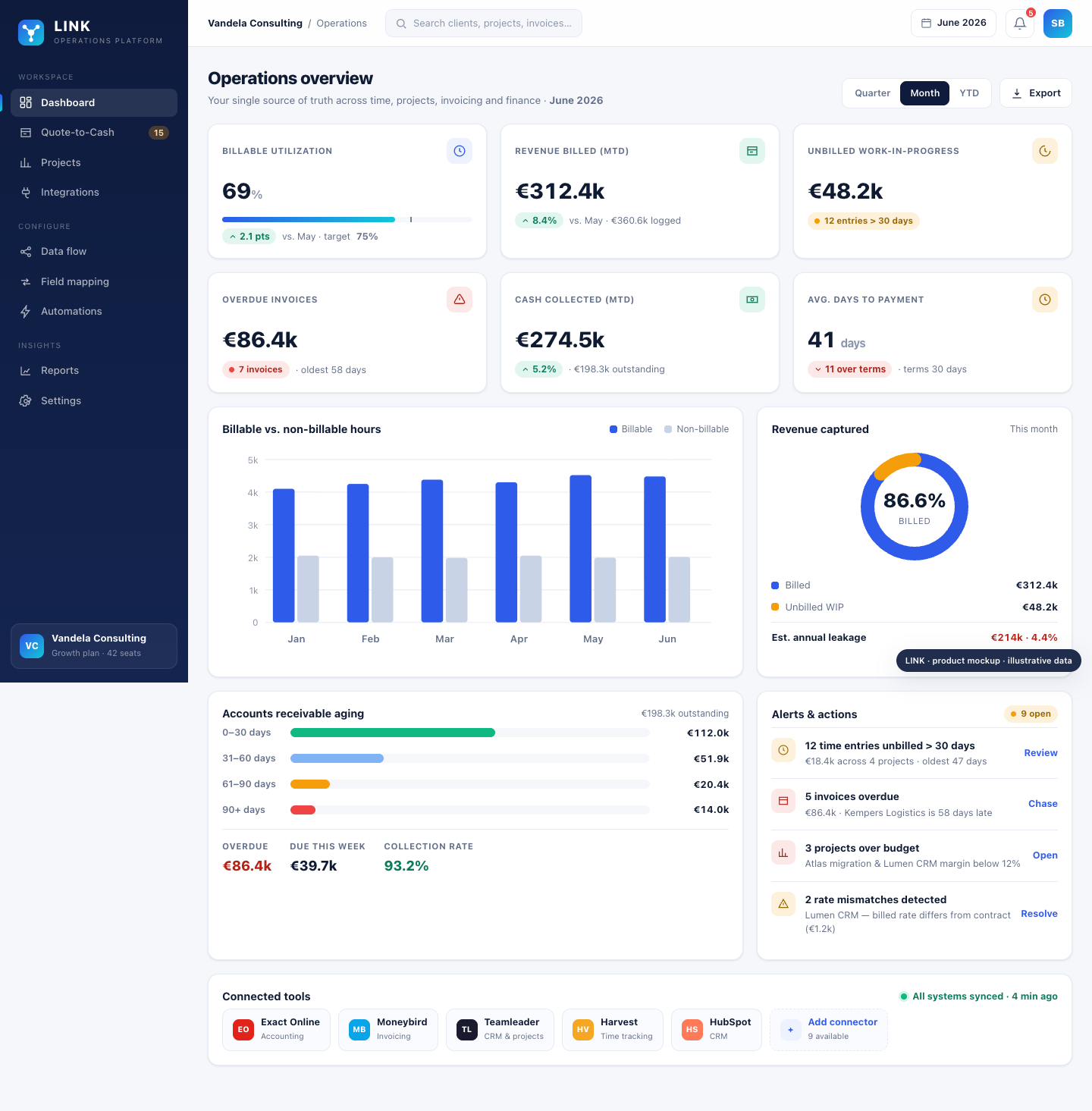

Product prototypes

Interactive screens showing how the concept becomes a usable product.

Set the deck up as a capstone defense, not only a pitch.

- Purpose: Show how the team moved from a broad operating-fragmentation problem to a focused business plan.

- Scope: Cover research, market selection, product prototype, operating model, financial assumptions and validation.

- Tone: The teacher should hear evidence, trade-offs and remaining risks.

- Transition: Move from concept excitement into business-plan discipline.